Optional Remuneration Arrangements – Cash Allowances & Salary Sacrifice

The draft legislation for Finance Bill 2017 has just been issued following the Chancellor’s Autumn Statement.

The Bill will change the way in which certain salary sacrifice schemes are taxed. Pensions, childcare, cycle to work and holiday salary sacrifice schemes are not affected.

The changes will also affect the taxation of cash alternative arrangements, e.g where an employee is given a choice of a cash allowance or a benefit such as a company car.

The details of the changes are as follows:

New provisions for the Finance Bill 2017 have been issued which will affect many salary sacrifice arrangements and all arrangements where an employee is offered a choice between a benefit and a cash alternative.

For salary sacrifice schemes, the main effect of the legislation will be to charge tax and employer’s NICs on the higher of the amount of the cash given up in a salary sacrifice scheme and the value of the benefit.

For cash alternative arrangements, e.g. where a choice of a company car or cash allowance is offered, tax will be charged on the higher of the benefit value and the cash alternative.

Pensions, childcare vouchers, cycle to work schemes and holiday salary sacrifice schemes will not be affected.

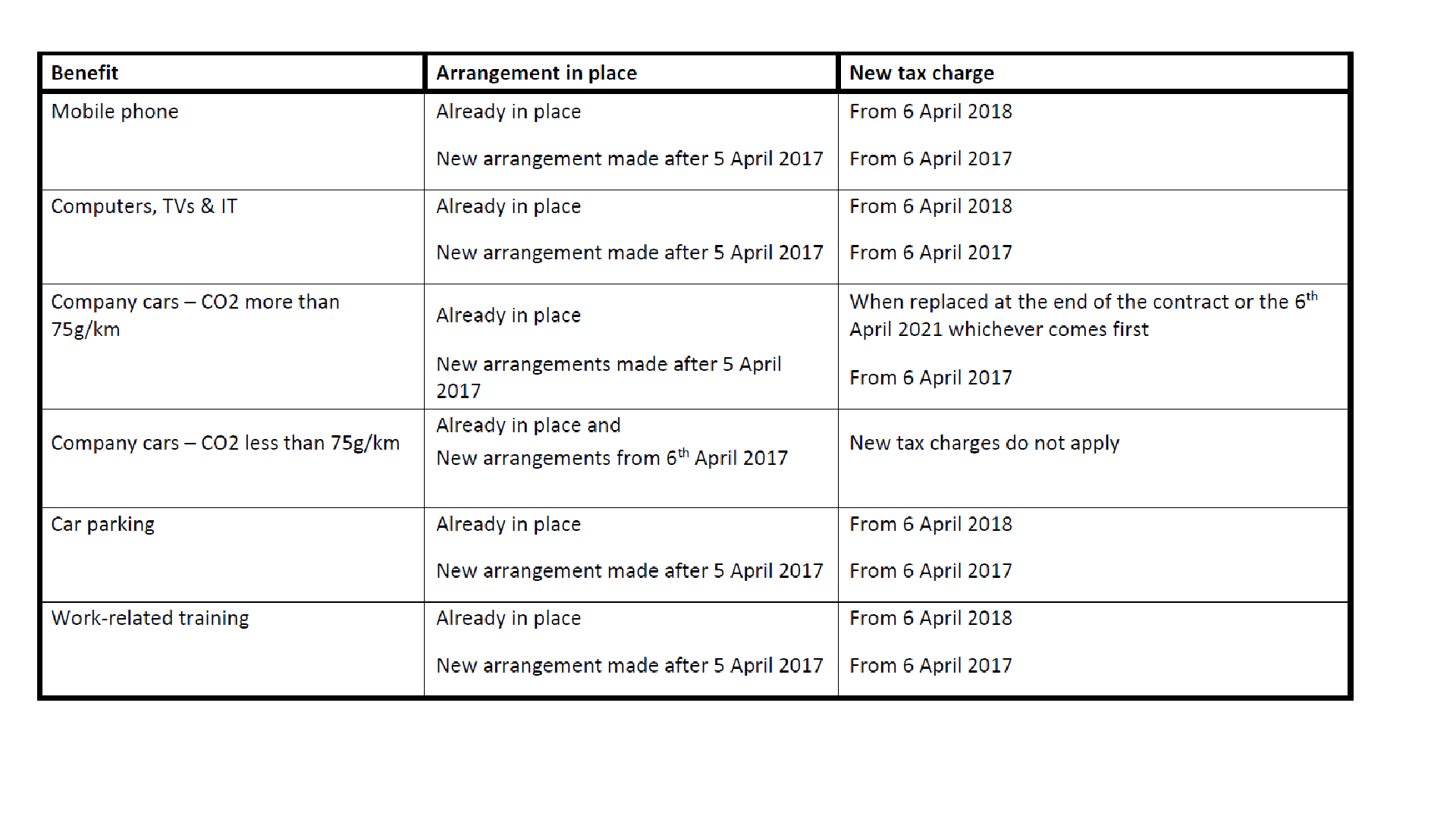

Tax –exempt schemes such as car parking and work-related training will become liable to tax and NICs from 6th April 2017 if they are provided under an Optional Pay Arrangement, i.e. a salary sacrifice scheme or a cash alternative arrangement.

One exception to the new legislation is for ultra- low emission cars with CO2s of less than 75g/km. These can continue to be provided under the current regime so that there will be savings of tax, employee and employer NIC, subject to a benefit in kind tax and class 1A NIC on the benefit.

It is worth noting that the changes don’t take away any of the soft benefits from salary sacrifice schemes, and the employees’ NICs saving is still there for all schemes.

Timing

The new legislation will affect all arrangements from 6th April 2017. The effect on any existing or new arrangements entered into between now and 5th April 2017 will be delayed to take effect from 6th April 2018 and for cars, vans, accommodation and school fees the delay will be extended to 6th April 2021.

This material is for informational purposes only and should not be relied upon as professional advice.