What is the issue?

This will apply to a business if they have one of the following:

- visitors from an overseas parent that visit the UK to assist in projects or ad-hoc work for the benefit of the UK business or

- visitors from a subsidiary or associated company that visit the UK to assist in projects or ad-hoc work for the benefit of the UK business.

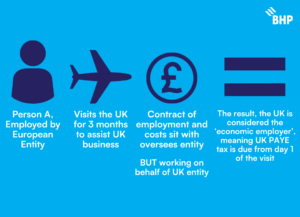

In the example above, the employer strictly speaking has a PAYE obligation that needs to be met, and this throws up several challenges around tracking the business visitor’s movements in and out of the UK, how to store this information and then ultimately get the payroll position correct. A further challenge could arise if the individual spends large amounts of time in the UK, as this may make them a UK tax resident.

What is the solution?

To prevent the administrative burden of HMRC having to deal with potentially lots of double tax relief claims, a HMRC agreement known as the Short-Term Business Visitor Agreement was borne.

The agreement allows for a relaxation of PAYE obligations for those coming to the UK from a country with which the UK has a double tax treaty (with the relevant employment income article). This means the UK-based entity does NOT need to include the international business visitor on the UK payroll and suffer tax that will only be repaid following a claim under the double tax treaty.

Note the following:

- The agreement is not applied automatically. Employers must approach HMRC to obtain this agreement (via a one-off application).

- The agreement only covers Income tax, it does not cover social security (National Insurance Contributions) which typically needs to be reviewed case by case based on the length of visit.

- Whilst it removes the payroll requirement, it is still necessary to track and monitor business visitors travel and this needs to be formally documented. There are different reporting requirements depending on the length of time an individual spends in the UK.

- Without obtaining this agreement from HMRC, strictly speaking PAYE applies from day 1.

- The annual report is due by 31 May following the tax year, i.e. a report for the year ended 5 April 2025 is due by 31 May 2025.

What actions may I need to consider?

- Do you have a non-resident director appointed to the UK Company? If so, the STBVA does not cover these individuals and other mechanisms are necessary to manage both personal tax and payroll positions (see Non-Resident Director article)

- Is the company confident that it can track its business visitors, including how much time they have spent in the UK and is there a process in place to capture and process this data?

- Understand who is coming to the UK, the nature of their visit and where they are coming from.

- Seek professional advice to understand your obligations and ways you can track business visitors.

- Apply for an STBVA with HMRC if you don’t have one!

If you would like to discuss the items in this blog, please contact us at info@bhp.co.uk

This material is for informational purposes only and should not be relied upon as professional advice.