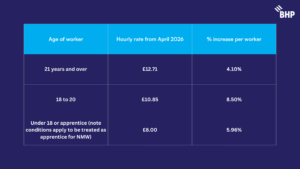

HMRC has announced that the following National Minimum Wage rates will apply to workers from pay periods commencing 1st April 2026.

The cost impact of the NMW increases will depend on the exact worker fact pattern, but below we have summarised illustrative examples for two main scenarios. Note that several assumptions have been applied, and the true costs may differ for your business. A list of our assumptions and caveats is outlined at the bottom of this blog.

Please note the change takes effect on the first pay period commencing on or after this date, so if you have a payroll spanning March and April, the date it applies may be later than 1st April 2026.

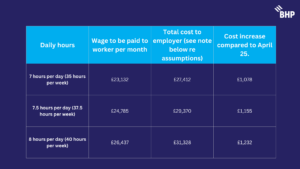

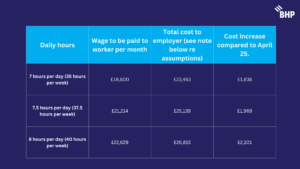

What is the impact to my business from April 26 if I pay workers by the hour?

For workers aged 21 or over (and not an apprentice)

The cost per worker is estimated to be:

For workers aged 18 to 20 (and not an apprentice)

The cost per worker is estimated to be:

For workers aged below 18 or an apprentice

The cost per worker is estimated to be:

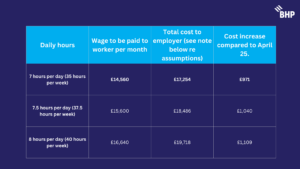

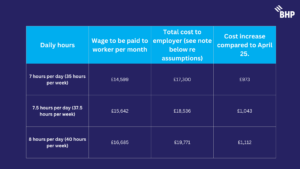

What is the impact to my business from April 26 if I pay workers a salary?

The rules are complex here and a worker for NMW could be treated as either salaried or unmeasured. For the purposes of demonstrating the impact we have assumed the worker is salaried.

For workers aged 21 or over (and not an apprentice)

The cost per worker is estimated to be:

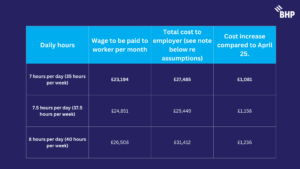

For workers aged 18 to 20 (and not an apprentice)

The cost per worker is estimated to be:

For workers aged below 18 or an apprentice

The cost per worker is estimated to be:

What else should I consider?

NMW enforcement

HMRC enforcement of NMW continues to increase and there are several technicalities which commonly lead to HMRC enforce employers to pay arrears to workers, plus penalties and public naming and shaming.

We recommend viewing HMRC guidance on common errors that lead to NMW arrears and seeking professional advice based on your circumstances.

There are simple steps that can be undertaken to clarify process or policy with workers that can prevent an unintended breach of the rules.

Salary sacrifice arrangements and deductions from pay

Salary sacrifice reduces pay for NMW purposes and deductions may also reduce pay for NMW purposes if the funds are held by the employer (and not passed to a third party).

What this means is the level to monitor NMW compliance is higher than the rates in the able above. So, make sure you payroll system checks the value after the salary sacrifice/deduction and NOT just the basic pay value.

Real living wage

This is a different rate set by the Living Wage Foundation and not to be confused with NMW. To comply you must pay the higher rate but note conditions are different and you could pay the real living wage and still breach NMW due to the technicalities highlighted in the government checklist.

Assumptions/caveats to illustrations outlined in this blog

- All amounts are rounded to nearest £

- Employer National Insurance contributions at 15%

- Employer pension contribution assuming a 3% contribution as per standard pension auto-enrolment schemes

- Apprenticeship levy of 0.5%. apprenticeship levy is due where you have annual pay bill of more than £3m. It still applies and is payable, even if you don’t pay employer NIC e.g. apprentices and under 21. See apprenticeship-levy

- No employer National Insurance (“NIC”) is due on workers below 21 or apprentices younger than 25 providing their pay is below the NIC upper secondary threshold NIC 25_26 rates

- Businesses can qualify for a corporate tax deduction for the costs incurred/paid on tax, wages and pensions. This would reduce the overall cost to the business and is not factored into the numbers in this article as rates vary and there is a time lag to recoup this cost back.

- We have assumed a multiplier of 52.14 weeks for salaried workers and 260 working days for time workers.

- Above calculations do not account for any differences that may apply in freeports and investment zones – note employer NIC applies on earnings lower than apprentices and under 25.

For more information, please contact our Tax team here.

This material is for informational purposes only and should not be relied upon as professional advice.