The start of 2024 has been an unusually busy time for UK reporters, with several fundamental changes on the horizon. In the Spring, the Financial Reporting Council (FRC) issued a major update to accounting standards used by most UK entities. There’s no single solution for each company, so we’ve set out below the key changes that will soon need to be considered by UK reporters.

FRS 102 – Triennial Update

Virtually all non-micro UK companies, LLPs and other entities will need to recognise numerical changes for periods beginning on or after 1 January 2026. The two major variations (leases and revenue) will both substantially align with International Financial Reporting Standards.

Leases

Virtually all leases will come onto balance sheet; the distinction between operating and finance leases is removed, and only short-term and leases of low-value assets are exempt (low value being by reference to the nature of the asset, not the value lease payments). This results in all lease assets and liabilities being recognised on the balance sheet. Download our detailed summary for further information.

Revenue

Revenue recognition will now be similar to the 5-step model of IFRS 15. More information can be found on our downloadable summary.

Impact on FRS 105

For micro-entities, the changes to revenue are broadly carried through to FRS 105. However, there is no requirement to recognise leases on balance sheet, which will create a material differential between micro and small companies. This may create a much stronger driver to choose FRS 105 over FRS 102 for micro-companies (subject to other changes noted on our detailed summary).

Small company disclosures

For those who meet the definition of a small company, the disclosure requirements have been significantly increased. Refer to our summary for full details.

Companies House filings

One area of ongoing uncertainty is around the final position arising from the Economic Crime and Corporate Transparency Act (ECCTA), which removed the option for companies to prepare abridged accounts entirely, as well as the option not to submit the Directors’ Report and Profit and Loss Account to Companies House. However, these are pending further government consultation.

Depending on the outcome, it’s notable that small companies will have to submit a P&L and add significant new disclosures around P&L metrics such as tax and dividends, where these previously didn’t need to be disclosed. We await confirmation of when this comes into force.

Size thresholds

For periods starting on or after 1 October 2024 (which can be of any length from 1 day up to 18 months), company size thresholds will also change. Refer to our summary for full details.

Proposals were made prior to the announcement of a General Election with plans to lay before parliament over the summer, thus timings and thresholds may well change from those announced.

It’s presumed that audit thresholds will continue to align with size thresholds, so any company meeting the micro or small definitions will be eligible for audit exemptions. No early adoption of new size thresholds is expected to be allowed.

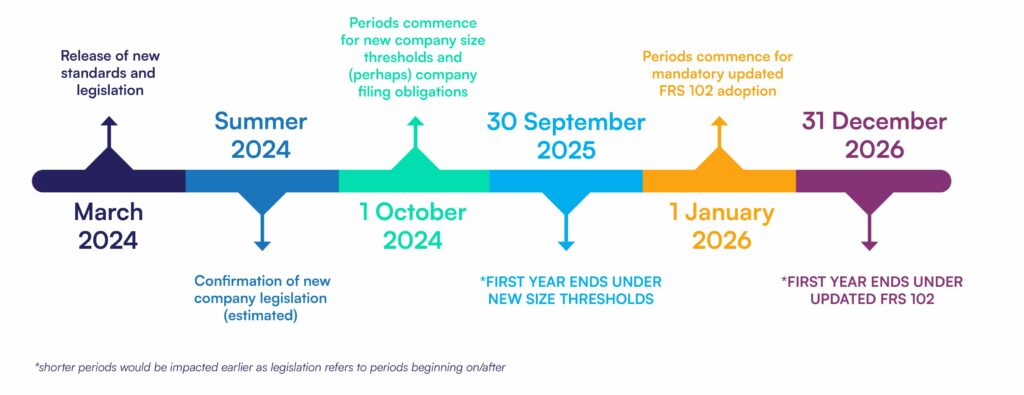

Predicted timeline

Actions

Actions

Clearly these changes are wide-ranging, and each entity needs to give careful consideration to its own circumstances. For many, these changes may drive a decision as to whether to report very little under a micro-entity regime, or lots under a small company regime; different sectors will be impacted differently here.

Your industry will also be key, and areas such as retail (where shops/units are typically leased) may suffer heavily from adding assets to the balance sheet and may even lose audit exemptions as a result. It is important to take advice tailored to your own circumstances and to plan for any changes (especially if you have covenants or expect to go through a major transaction such as a sale in the next few years).

Please get in touch with Alex Hird in our Financial Reporting, Advisory and Valuations team for any initial discussions and queries around this topic.

Note – this is written in general terms but should not be relied upon as explicit advice for any individual or entity and includes statements which we believe to be correct as at the date of publication only. It is highly likely that future changes to this blog post will be required. To the greatest extent permitted by law we do not accept any liability from any party who acts on, or fails to act on, any generic guidance given in this document. We would be happy to support entity with an individual impact assessment and tailored advice to its circumstances.

This material is for informational purposes only and should not be relied upon as professional advice.