Major reforms to Statutory Sick Pay (SSP) are on the way, with the Employment Rights Bill introducing some of the biggest changes we’ve seen in years. These updates aim to make sick pay fairer and more accessible, but they also mean new costs and considerations for employers.

Here’s what you need to know:

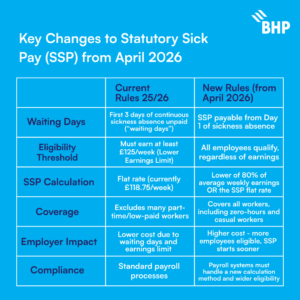

1. No More Waiting Days

Currently, the first three days of continuous sickness absence are unpaid. From April 2026, these “waiting days” will be abolished, and SSP will be payable from day one of absence.

2. All Employees Will Qualify

Currently, workers must earn at least £125 per week to qualify for SSP. This Lower Earnings Limit will be removed entirely, allowing all employees, including part-time, low-paid, casual, and zero-hours workers, to receive SSP.

3. New SSP Calculation Method

The traditional flat-rate system (currently £118.75 per week) is changing.

From April 2026, employers must pay the lower of:

-

80% of the employee’s average weekly earnings, or

-

The standard SSP flat rate.

The flat rate will remain as a cap and continue to be uprated annually.

Payroll and Compliance Updates

Payroll teams will need to update systems to:

-

Apply the new calculation method

-

Remove waiting days

-

Manage wider employee eligibility

Importantly, employers still cannot reclaim SSP from the government (unlike maternity pay), so budgeting and forecasting will be key.

What This Means for Employers

These reforms are designed to modernise sick pay and support more workers, but they’ll bring real financial and operational impacts. Now is the time for employers to review payroll processes, model potential costs, and prepare for a more inclusive SSP framework.

For more information, contact our payroll team here.

This material is for informational purposes only and should not be relied upon as professional advice.